Introduction

Trying to get help for depression is hard enough. Adding insurance billing confusion on top of it can feel impossible. If you have ever stared at an Explanation of Benefits form and felt your stomach drop, you are not alone.

Here is the thing: the complexity of mental health billing services actually stops many people from getting the care they need. In 2024, nearly 10% of U.S. adults with mental illness had no insurance coverage at all, according to NAMI. And even for those with insurance, finding a provider who accepts it is a real challenge. A 2026 report from the American Hospital Association found major gaps in in-network mental health coverage. On top of that, insurance reimbursements for behavioral health visits are on average 22% lower than for medical visits, according to a study cited by APA Services.

These numbers are not just statistics. They represent real people putting off treatments for mental health issues because the billing side feels too confusing or expensive.

But here is the good news. When you understand a few key billing concepts, the whole process becomes much less scary. Knowing what terms like deductible, copay, and out-of-network mean gives you confidence. It helps you ask the right questions. For example, learning how a specific insurer handles claims can make a big difference, like in our guide to Cigna mental health coverage.

This article gives you a clear, step-by-step roadmap to navigating mental health insurance in 2026. We will cover how to check your coverage, what to do if your therapist does not take your insurance, and how to identify strategies to reduce barriers to accessing mental health support. Let us start by understanding what you are working with. As you build this knowledge, remember that small healthy habits can lighten the load. One innovative program that rewards positive behaviors was highlighted by Authority Magazine for its ability to offset anxiety and depression.

Why Mental Health Billing Matters: The Role of Insurance

Your insurance plan can be the biggest reason you start or stop getting help for depression. If you have ever had to choose between seeing a therapist and paying rent, you know exactly how heavy that weight feels. That is why understanding how mental health billing services work is not just paperwork. It is about opening the door to the care you need.

The good news is there is a federal law on your side. The Mental Health Parity and Addiction Equity Act (MHPAEA) says that insurance plans must treat mental health coverage the same as physical health coverage. That means copays, deductibles, and visit limits should be equal. The American Psychological Association explains that you can check your plan’s benefits to see if it follows these rules. For example, if your plan only allows 30 physical therapy visits a year but only 10 therapy visits, that could be a violation.

But here is the thing. Even with the law, lots of people still hit roadblocks. Many insurance plans have high deductibles before they start paying for mental health care. Others have very small networks of therapists who accept the plan. A guide from Mental Health America notes that your insurance company can give you a list of in-network providers. But that list might be short or include providers who are not taking new patients. That is one of the biggest barriers to getting consistent treatments for mental health issues.

So what can you do? First, call your insurance and ask specific questions about your mental health benefits. Ask about your deductible, copay, and how many sessions are covered. This is part of understanding how money flows through the system. A beginner’s guide to mental health billing explains that knowing the basics of billing helps you avoid surprises and choose the right provider.

If you live in a state like California, you may have access to public programs that can help. For instance, you can find the CA Medi-Cal phone number for mental health services to check what public insurance covers.

Ultimately, understanding the role insurance plays helps you identify strategies to reduce barriers to accessing mental health support. You can plan ahead, ask the right questions, and push for the care you deserve.

Key Insurance Terms Every Mental Health Patient Should Know

Now that you understand how insurance shapes your access to care, let’s talk about the words your insurance company uses. Terms like deductible, copay, coinsurance, and out-of-network can feel like a foreign language. But here’s the truth. Learning just a few of these terms can save you hundreds of dollars and a lot of frustration.

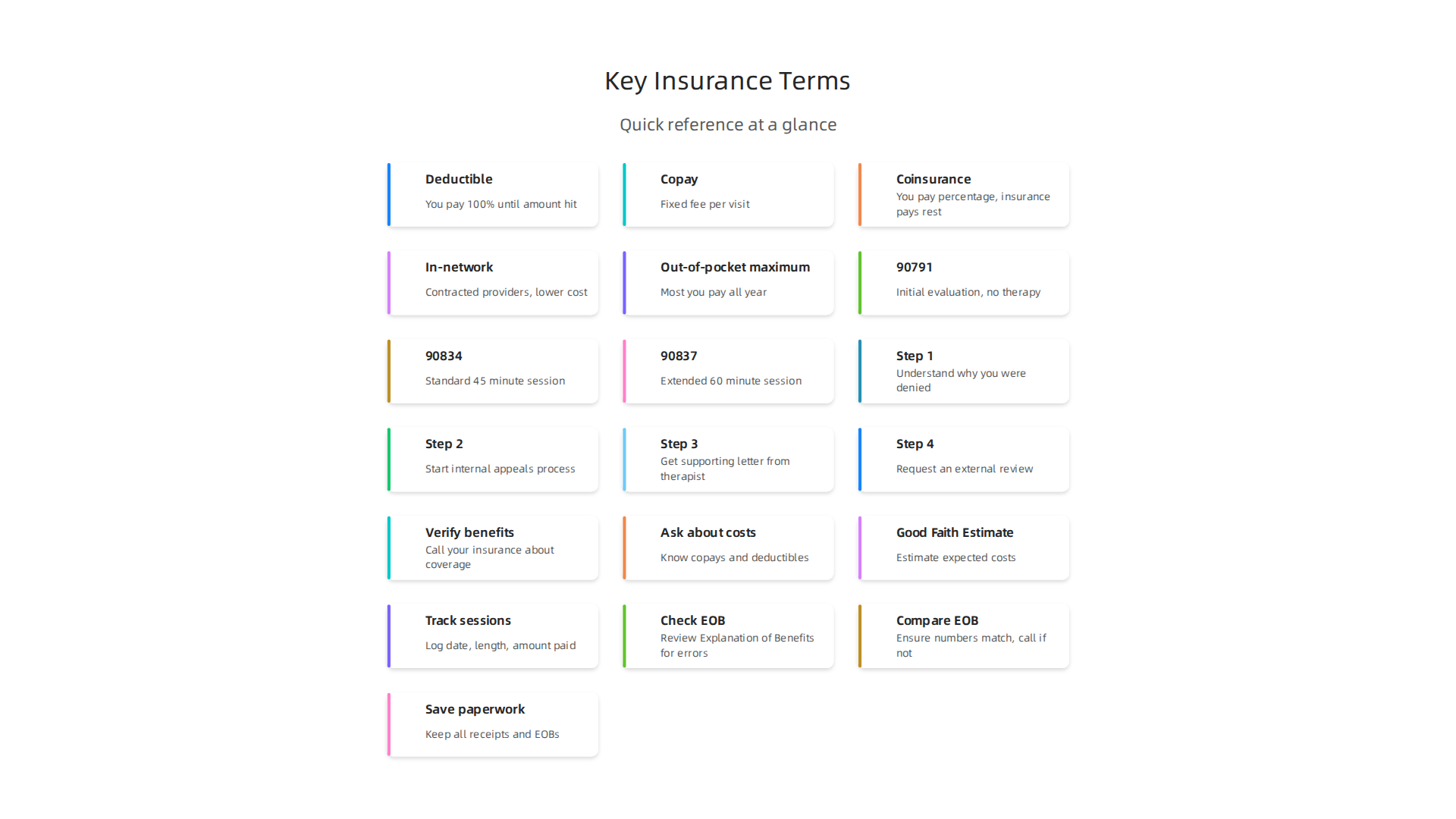

Deductible

This is the amount you pay each year before your insurance starts paying. For example, if your plan has a $2,000 deductible, you pay the full cost of your therapy sessions until you have spent $2,000. After that, your insurance kicks in. A guide from Solmental Health recommends reviewing your benefits first so you know exactly what your deductible is before booking your first appointment.

Copay

A copay is a fixed fee you pay each time you see a provider. It might be $25 or $40 per session. Copays usually apply after your deductible is met, but some plans offer copays from day one. Always check.

Coinsurance

Coinsurance is different. Instead of a fixed fee, you pay a percentage of the cost. If your coinsurance is 20%, and the session costs $150, you pay $30. The insurance pays the rest. This percentage applies after your deductible.

In-network vs. out-of-network

This is a big one. In-network providers have a contract with your insurance company. They charge lower rates. Out-of-network providers do not have a contract. You usually pay much more out of pocket. Mental Health America explains that your insurance company can give you a list of in-network providers. Stick with that list when possible.

Annual out-of-pocket maximum

This is your safety net. The out-of-pocket maximum is the most you will pay in a year for covered in-network care. Once you hit that limit, your insurance pays 100%. For someone getting regular treatments for mental health issues, this cap can be a lifesaver.

If you want a full breakdown of how these terms work together, the complete beginner’s guide to mental health billing walks through everything step by step.

Understanding these terms helps you identify strategies to reduce barriers to accessing mental health support. You can ask smarter questions when you call your insurance company. You can compare plans during open enrollment. And you can choose a provider who fits your budget.

If you live in a state like California and use public insurance, you can also find helpful info about how to use your specific benefits like the CA Medi-Cal phone number for mental health services.

Each term you learn is one less barrier between you and the care you need.

Quick reference table: Key insurance terms at a glance

| Term | What it means in simple words |

|---|---|

| Deductible | You pay 100% until you hit this amount |

| Copay | Fixed fee per visit, often $20-$50 |

| Coinsurance | You pay a percentage, insurance pays the rest |

| In-network | Providers with a contract, lower cost to you |

| Out-of-pocket maximum | The most you will pay all year, then insurance covers everything |

How to Verify Your Mental Health Insurance Coverage

You now know the language of insurance. But talking is not enough. You need to act. The best time to verify your coverage is before you book your first appointment. A simple phone call can prevent surprise bills and help you feel in control.

Here is the honest truth. A ten minute call can save you from a $200 shock later. You would not buy groceries without checking the price. Therapy is the same. You deserve to know what you will pay before you start your healing journey.

Start with the right phone call

Call the number on the back of your insurance card. Ask for the behavioral health department. General customer service reps sometimes give wrong answers about mental health. Then ask these specific questions:

- Have I met my deductible? If yes, your coverage starts right away.

- What is my copay or coinsurance? Know the exact dollar amount or percentage.

- How many sessions are allowed? Some plans cap you at 20 or 30 visits per year.

- What is my out-of-pocket maximum? This is your safety net.

If you use a plan like Elevance Health, call the number on your card and ask these exact questions.

Know your legal rights

In 2026, federal law has your back. The No Surprises Act says that if you pay without using insurance, your provider must give you a Good Faith Estimate. This paper shows the full expected cost of your care. CMS provides the billing standards that keep these estimates honest and accurate.

For a standard therapy session, your therapist might use CPT code 90834. MedSolercm explains that this is the most common code for a 45 minute session. Knowing the code helps you sound confident when you talk to your insurance company.

Use your verification to save money

Once you know your numbers, you can make smart choices. If your copay is too high, ask about a sliding scale fee. If your plan limits sessions, look for short term therapies.

If you live in a state like California, you can find the CA Medi-Cal phone number for mental health services for state specific help. If you have a plan like Cigna, check out this guide on Cigna mental health coverage to understand your benefits better.

Reduce your barriers to care

Knowing your benefits helps you identify strategies to reduce barriers to accessing mental health support.

You can choose a therapist who fits your budget. You can pick a treatment style that works with your session limits. For example, Cognitive Behavioral Therapy for panic attacks is often short term and very effective.

You can also ask a clinic’s billing team for help. Many mental health billing services will check your benefits for you. They want the claim to go through, so they are usually happy to help.

Stay on track with your healing

Once your coverage is sorted, you need to stay engaged in your treatments for mental health issues. A great external resource for understanding how to stick with your goals is the peer white paper The Science of Gamification. It breaks down the behavioral science behind staying motivated.

Verifying your insurance is not just about money. It is about peace of mind. When you know you are covered, you can relax into your sessions. You can focus on what truly matters: getting better.

Understanding Mental Health Billing Codes (CPT Codes)

You made the call. You checked your deductible and copay. Now you need to understand the secret language your insurance company uses. That language is CPT codes.

CPT stands for Current Procedural Terminology. These are five digit numbers that describe the service you receive. Every therapy session, evaluation, or psychiatric visit gets a code. Your insurance uses these codes to decide what to pay.

Here is the thing. If the wrong code is used, your claim gets denied. A simple mistake can cost you hundreds of dollars. That is why understanding a few key codes puts you in control.

**The most common CPT codes for therapy

**

According to the 2026 billing guidelines from CMS, psychotherapy codes range from 90832 to 90838. But you really only need to know three.

| Code | Session Length | What It Covers |

|---|---|---|

| 90791 | First session only | Initial evaluation, no therapy |

| 90834 | 38 to 52 minutes | Standard 45 minute session |

| 90837 | 53 minutes or more | Extended 60 minute session |

Code 90834 is the most frequently billed code for outpatient therapy. MedSolercm explains that this code covers your typical weekly session. Code 90837 is for longer sessions. HealthArc notes that 90837 requires at least 53 minutes of face to face time.

Why the exact time matters

Your therapist must document the time carefully. If they bill 90837 for a 45 minute session, the claim might get rejected. EliteMed Financials warns that you should bill the code whose time range your session actually falls within. Not the one that pays more.

This is where professional mental health billing services can help. They make sure codes match the actual time spent with your therapist. If you use a plan like Elevance Health, a billing specialist can double check everything before it goes to your insurance.

How to use this knowledge

When you book a session, ask your therapist what code they will use. Ask how long the session will be. If you want a 60 minute session, confirm they will use 90837. If your plan only covers 45 minutes, stick with 90834.

This simple question can prevent a surprise denial. It is part of how you identify strategies to reduce barriers to accessing mental health support. Knowledge is power here.

If you live in a rural area or have trouble finding providers, check out this guide on navigating the Missouri Department of Mental Health to find local services that accept your insurance.

The bottom line on CPT codes

You do not need to memorize every code. But knowing 90834 and 90837 helps you sound confident when you call your insurance. It helps you ask better questions. And it helps you avoid billing mistakes that delay your treatments for mental health issues.

Your therapy time is precious. Make sure every minute is coded correctly.

In-Network vs Out-of-Network: Costs and Considerations

So now you know the codes your therapist will use. But the next big question is whether your therapist is in-network or out-of-network with your insurance. This choice can change your bill by hundreds of dollars.

Here is the simple difference. An in-network provider has a contract with your insurance company. They agreed to a set price for each session.

That price is usually lower than what you would pay without insurance. Your insurance also covers a bigger chunk of the cost.

An out-of-network provider has no contract with your insurance. They can set their own price. And here is the tricky part. Your insurance may still pay something, but at a much lower rate than if the therapist were in-network.

The biggest risk with out-of-network care

The term you need to know is balance billing. When you see an out-of-network therapist, they may charge you more than what your insurance says is reasonable. Your insurance pays their share based on their own price list. Then the therapist bills you for the rest. You owe the full difference.

According to NAMI, treatment for mental illness can be denied or limited by insurance companies for various reasons. But out-of-network denials happen more often than you might think. Claim denials related to eligibility and authorization are also common, as Prosperity Behavioral Health explains.

What to check before you book

Call your insurance and ask three questions:

- Is this therapist in-network?

- If not, what percentage of out-of-network costs do you cover?

- Is there a separate deductible for out-of-network care?

Some plans, like Elevance Health, offer a mix of both options. But the lower your out-of-network benefits, the more you pay yourself.

If you are choosing a therapist, start with in-network providers. This is one of the best ways to identify strategies to reduce barriers to accessing mental health support and get treatments for mental health issues without a surprise bill later.

For more help finding the right provider, check out this guide on Cigna mental health coverage to understand how different plans work.

The bottom line

In-network means predictable, lower costs. Out-of-network gives you more choice but also more risk. Know which one you have before you start therapy. Your wallet will thank you.

What to Do If Your Mental Health Claim Is Denied

Getting a denial letter from your insurance company can feel like a punch in the gut. You finally found a therapist you trust. You are putting in the work. And then the system says no. But here is the truth: denials are common, and they are not always the final answer.

The most frequent reason insurance companies deny mental health claims is by saying the treatment was “not medically necessary.” According to the DL Law Group, this is the number one reason in 2026. Other common reasons include missing pre-authorization, incorrect coding, and billing errors. Prosperity Behavioral Health lists incomplete documentation and eligibility issues as top triggers.

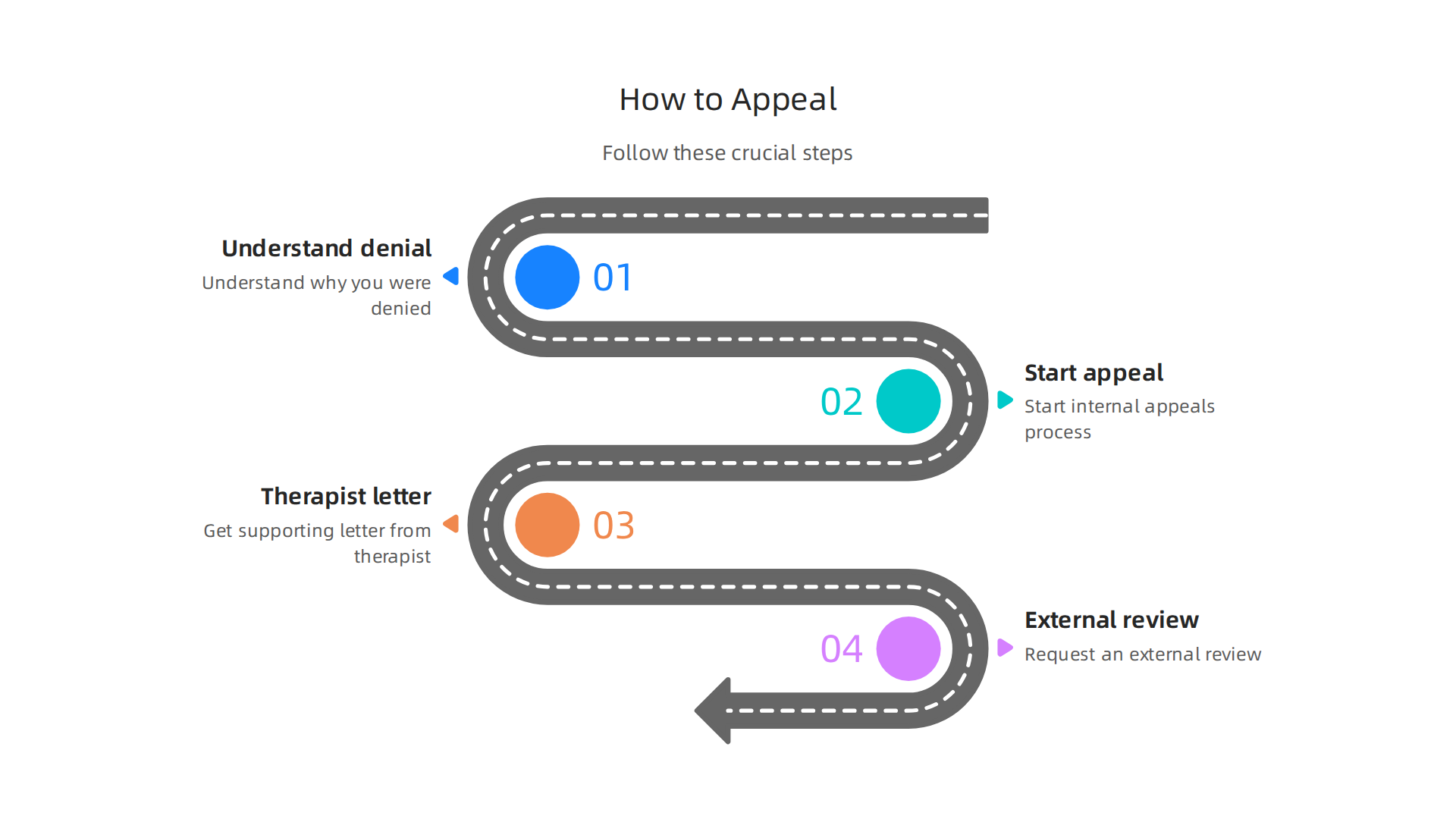

So what do you do next?

Step 1: Understand why you were denied

Read the denial letter carefully. It will usually list a reason code or a short explanation. Common ones include “services not covered,” “authorization not obtained,” or “out-of-network provider.” If you spot a coding error, your therapist can often resubmit with the correct code.

Step 2: Start the internal appeals process

Every insurance plan has an internal appeal process. You have the right to ask the company to review its decision. Make sure you submit your appeal within the time limit written on your denial letter. The National Alliance on Mental Illness (NAMI) recommends sending your appeal by certified mail so you have proof of delivery.

Step 3: Get a supporting letter from your therapist

This is one of the most powerful tools you have. Ask your therapist to write a detailed letter explaining why the treatment is medically necessary. They should describe your symptoms, the diagnosis, and how therapy directly treats the condition. This letter alone can turn a denial into an approval.

Step 4: Request an external review

If the internal appeal fails, you can request an external review. An independent third party looks at your case. This is often your last chance, and it beats accepting a denial.

If all of this sounds overwhelming, you do not have to face it alone. Professional mental health billing services can handle the paperwork and appeals for you. They know the rules and the codes. They can also help you identify strategies to reduce barriers to accessing mental health support so you focus on your healing.

For example, you can learn more about how your plan works with this guide on Cigna mental health coverage. And if you are looking for ways to build resilience and avoid future denials by strengthening your support system, check out this Youth Safety Case Study which shows how early reinforcement helps protect against mental health struggles.

The bottom line

A denial is not the end. It is a step in the process. Know your rights, get your therapist’s help, and keep pushing. Your mental health is worth the fight.

Strategies to Reduce Out-of-Pocket Mental Health Costs

You’ve handled the denial and now you want to afford care without the insurance stress. Great news: there are real ways to lower what you pay out of pocket. You don’t have to skip therapy just because your plan is confusing or your deductible is high.

Sliding scale fees

This is one of the most common options. A sliding scale means the therapist lowers their price based on your income and family size. Many therapists set up a flexible fee schedule, so you pay what you can afford. Psychology Today explains that sliding scale payments are an agreement between you and the provider to pay a reduced rate. It’s worth asking every therapist you call if they offer a sliding scale. Some clinics, like Burrell Behavioral Health, offer discounted fees for those who qualify.

Community mental health centers

Local community health centers often provide therapy at low or no cost. The Substance Abuse and Mental Health Services Administration (SAMHSA) lists many centers that use a sliding fee scale. You can call them directly to see if you qualify.

Cash-pay discounts

Some therapists charge less if you pay with cash instead of filing insurance. They avoid the paperwork hassle, and you save money. If you have a high deductible plan, this can be cheaper than using your insurance. Just be sure to ask about it upfront.

Employee Assistance Programs (EAPs)

Your job may offer free counseling through an EAP. Most EAPs give you 3 to 8 free sessions per year. That’s a great way to start treatment without any cost. Check with your HR department to see what’s available.

Nonprofit organizations

Groups like local mental health nonprofits and religious organizations sometimes offer free or cheap therapy. You can search online or call a resource line in your area.

If managing all these options feels like too much, a professional mental health billing service can help you identify strategies to reduce barriers to accessing mental health support. They know which programs exist and how to apply. You can also explore more resources like this guide on finding low-cost mental health services through Medi-Cal if you live in California.

The bottom line: you can find affordable treatments for mental health issues if you know where to look. It takes a few calls or clicks, but the help is out there.

Your Step-by-Step Checklist for Navigating Billing

You already know the strategies to lower costs. But even with discounts and sliding scales, you still need to handle the paperwork. This checklist makes it simple. Follow these steps before, during, and after treatment to avoid surprise bills.

Before your first session

This is where most people make mistakes. Do these three things before you even sit down with your therapist.

-

Verify your benefits. Call your insurance or log into your online account. Ask about mental health coverage specifically. Not all plans cover therapy the same way. Some require preauthorization. Some only cover certain types of providers. Double check everything before you book.

-

Ask about copays and deductibles. Know exactly how much each visit will cost you. If you have a high deductible plan, you may pay the full fee until you hit that deductible. Get the dollar amount in writing if you can.

-

Request a Good Faith Estimate. This is your right under federal law. Providers must give you an estimate of expected costs before you start treatment. This helps you plan and avoid surprises. The SAMHSA resource on free and low-cost treatment can guide you to providers who respect your budget.

During treatment

Stay on top of your paperwork month by month.

- Track your sessions. Keep a simple log with the date, length of session, and amount paid. A notebook or a notes app works fine.

- Check your Explanation of Benefits (EOB) every time you get one. Your insurance sends these after each claim. Look for errors. Did they pay the right amount? Did they apply your copay correctly? Mistakes happen more often than you think.

- Compare your EOB to your receipts. If the numbers don’t match, call your insurance right away.

After treatment ends

You are not done yet. Save every receipt and every EOB for at least one year. If a claim gets denied, you can appeal. A denial does not mean you lose. It often means someone coded something wrong. With the right paperwork, you can fix it.

If managing all this feels overwhelming, professional mental health billing services can handle the details for you. They know how insurance works and can spot errors quickly. You can also learn more about coverage specifics in this guide on Cigna mental health coverage and therapy costs.

This checklist is your shield. Use it with every provider, every claim, and every bill. It keeps you in control so you can focus on what really matters: your healing.

Summary

This article is a practical roadmap to navigating mental health billing in 2026 so you can find, afford, and keep getting the care you need. It explains why insurance choices and laws like parity matter, then breaks down essential terms—deductible, copay, coinsurance, in-network versus out-of-network, and out-of-pocket maximums—so bills stop feeling like a mystery. You’ll learn how to verify benefits with your insurer, ask the right questions, and use CPT codes (especially 90834 and 90837) to avoid claim denials. The guide also covers what to do if a claim is denied, ways to lower costs (sliding scale, community clinics, EAPs, cash-pay), and a simple before-during-after checklist to prevent surprises. Throughout, the emphasis is on concrete steps and resources that reduce barriers to treatment and help you focus on recovery.