Why Understanding Your Cigna Mental Health Coverage Matters

You want to feel better. Maybe you have been thinking about talking to a therapist for a while. But a big question always holds you back: How much will it cost? This worry keeps a lot of people from getting the help they need.

You pay for health insurance every month. If you have a plan through work or bought one yourself, you likely have Cigna. That means your plan probably already includes cigna mental health coverage. But here is the thing: most people never check what their plan actually covers. And that is a huge problem.

In 2026, money feels tighter than ever. Healthcare costs are going up across the board. Without knowing the ins and outs of your mental health insurance coverage and plans, it is very easy to overpay. You might choose a therapist who is out of network when an in-network option is just as good and costs much less. You might even skip care completely because you are afraid of a surprise bill in the mail.

The good news is that Cigna covers therapy and counseling as part of your standard medical plan. You can check Cigna’s mental health and substance use benefits page for official details. Knowing the difference between in-network and out-of-network providers is what saves you real money. For a deeper look at copays and deductibles, read through this guide to Cigna mental health coverage: what you need to know about therapy and costs.

Let us take a close look at your plan together. We will cover exactly what is included, what it costs, and how to get the most out of your benefits without stress. Feeling emotionally drained? The pressure may not be only personal. Understanding your coverage is a practical step toward feeling more in control. Feeling Emotionally Drained?

Let us start.

What Does Cigna Mental Health Coverage Include?

The best way to start is by understanding exactly what your plan covers. Cigna mental health coverage is broad, but the details matter a lot. Your mental health benefits are part of your regular medical plan. There is no separate insurance card for therapy. Your Cigna Healthcare Individual and Family Plan Benefits page shows exactly what is included in your specific policy.

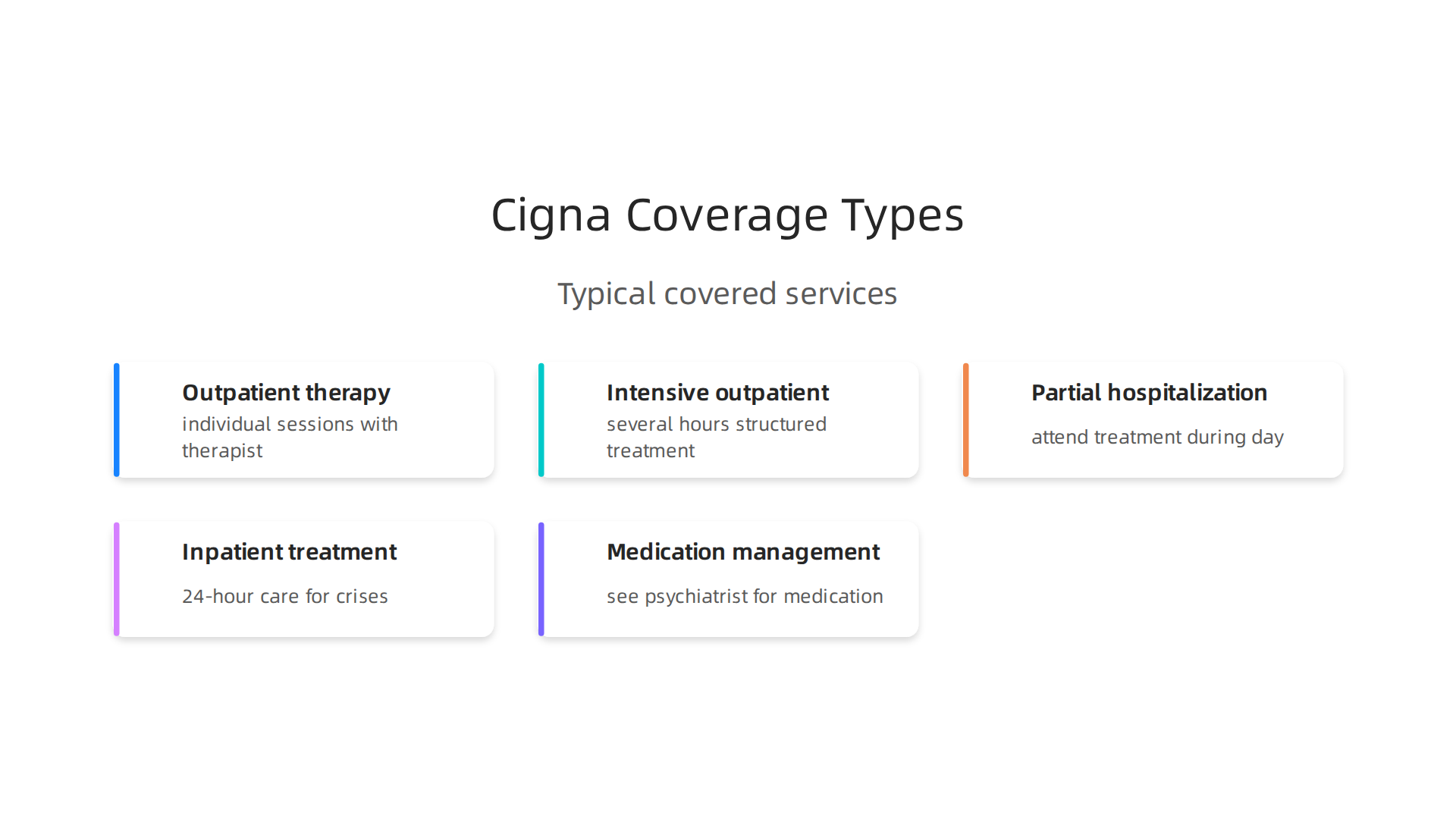

Most Cigna plans cover a wide range of services. Here is what you can typically expect:

- Outpatient therapy. This covers individual sessions with a therapist, group therapy, and family counseling. These are the most common types of care people use. Depending on your plan, an in-network session usually costs between $20 and $50 as a copay.

- Intensive outpatient programs (IOP). If you need more support than weekly therapy, an IOP gives you several hours of structured treatment each week while you still live at home.

- Partial hospitalization programs (PHP). This is a step up from IOP. You attend treatment during the day and return home at night.

- Inpatient mental health treatment. For serious situations where you need 24-hour care, Cigna covers hospital stays for mental health crises.

- Medication management. If you see a psychiatrist for medication, that is also covered under your plan.

The exact cost you pay depends on whether you see an in-network or out-of-network provider. Cigna Out-of-Network Benefits: Mental Health & Therapy explains how out-of-network care works. In general, staying in network saves you a lot of money.

Here is a key point: the Affordable Care Act requires all plans to cover mental health as an essential health benefit. So your plan definitely includes these services. But the details vary by employer. Your specific copay, deductible, and out-of-pocket maximum depend on the plan your employer chose. For a deeper look at managing costs and avoiding billing headaches, read through this guide on how to navigate mental health insurance billing and afford therapy in 2026.

No matter your plan, the most important step is checking what your specific Cigna policy covers before you book an appointment. That way, you avoid surprises and get the care you actually need.

In-Network vs. Out-of-Network Providers: Key Cost Differences

Now that you know what your Cigna plan covers, the next big question is who you see. Choosing between an in-network and out-of-network therapist can change your bill by hundreds of dollars.

So let’s break it down simply.

In-network providers have signed a contract with Cigna. They agree to charge a set rate that Cigna negotiated. That rate is usually 30 to 60 percent lower than what an out-of-network therapist charges. Your share is just a copay of $20 to $50 per session, or a small percentage after you meet your deductible. The Cigna Mental Health Coverage & Benefits Guide explains these cost differences in more detail.

Out-of-network providers do not have a contract with Cigna. You pay the full fee upfront, then file a claim to get some money back. Here’s the catch: the amount Cigna reimburses is based on their own maximum rate, not what the therapist actually charges. So you could end up paying a lot more out of pocket. And in many plans, out-of-network spending does not count toward your out-of-pocket maximum. That means you could keep paying all year without hitting your cap. For a full breakdown of how this works, check out the Does Cigna Cover Mental Health Therapy? Coverage Explained article.

Cigna offers a provider search tool on their website to help you find in-network therapists near you. But here is a reality check many people face: lots of those listed providers are not accepting new patients. You may need to call several before you find an opening. That can feel discouraging, especially when you already need support.

If you are feeling stuck or frustrated by the search process, you are not alone. The emotional weight of navigating insurance and finding care can be draining. Feeling Emotionally Drained? The pressure may not be only personal. It is okay to take a step back and prioritize your well-being first.

For practical help finding the right professional, our guide on amp mental health providers guide to psychiatrists therapists and counselors walks you through the different types of providers and how to match them to your needs. Knowing the difference between a psychiatrist, psychologist, and therapist can save you time and money.

The bottom line is simple: staying in network saves money and hassle. But finding an available in-network therapist takes some patience. Start with Cigna’s tool, call a handful of names, and don’t give up after the first no.

How to Verify Your Cigna Mental Health Benefits for Therapy

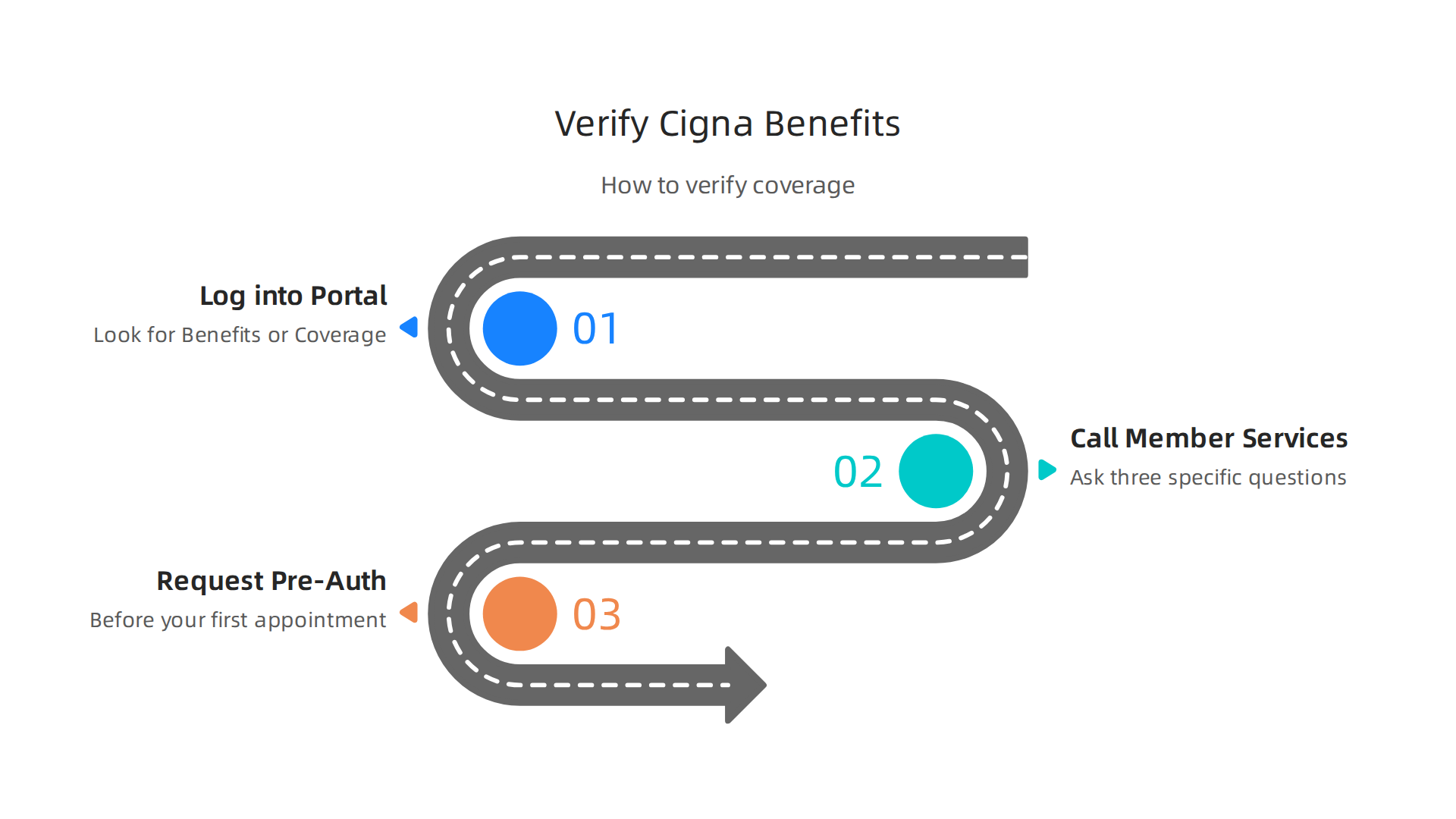

So you’ve started searching for an in-network therapist using Cigna’s tool. Good first step. But the next move is just as important: you need to know exactly what your specific plan covers. Not all Cigna plans are the same. The details live in your policy, not in a general brochure. Here is how to find them.

First, log into the Cigna portal or download the Cigna app.

Once you are in, look for a section called "Benefits" or "Coverage." You should see a mental health or behavioral health category. Click it. This screen will show your copay, deductible, and session limits for therapy. It may also list covered services like individual therapy, group therapy, and telehealth. For a full walkthrough of what to look for, check out the Cigna Mental Health Coverage Guide.

Second, call the member services number on the back of your insurance card. Have your card ready. Ask three specific questions:

- What is my copay for an in-network therapy visit?

- How many sessions are covered per year?

- Do I need a pre-authorization after a certain number of sessions?

Many Cigna plans require pre-authorization for ongoing therapy beyond a set number of visits. If you skip this step, you could get a surprise bill later. So write down the name of the person you speak with and the reference number for your call.

Third, if your plan does require pre-authorization, request it before your first appointment. Your therapist’s office can help with this. They will submit paperwork to Cigna explaining why you need therapy. Once approved, you are clear to continue treatment without worrying about denied claims.

Verifying your benefits now saves you headaches later. For a deeper look at how insurance billing works for mental health, read our guide to navigating mental health insurance billing. It covers common pitfalls and how to avoid them.

The whole process takes about 20 minutes. Do it before you book your first session, and you will step into therapy knowing exactly what to expect financially.

Understanding Copays, Coinsurance, and Deductibles

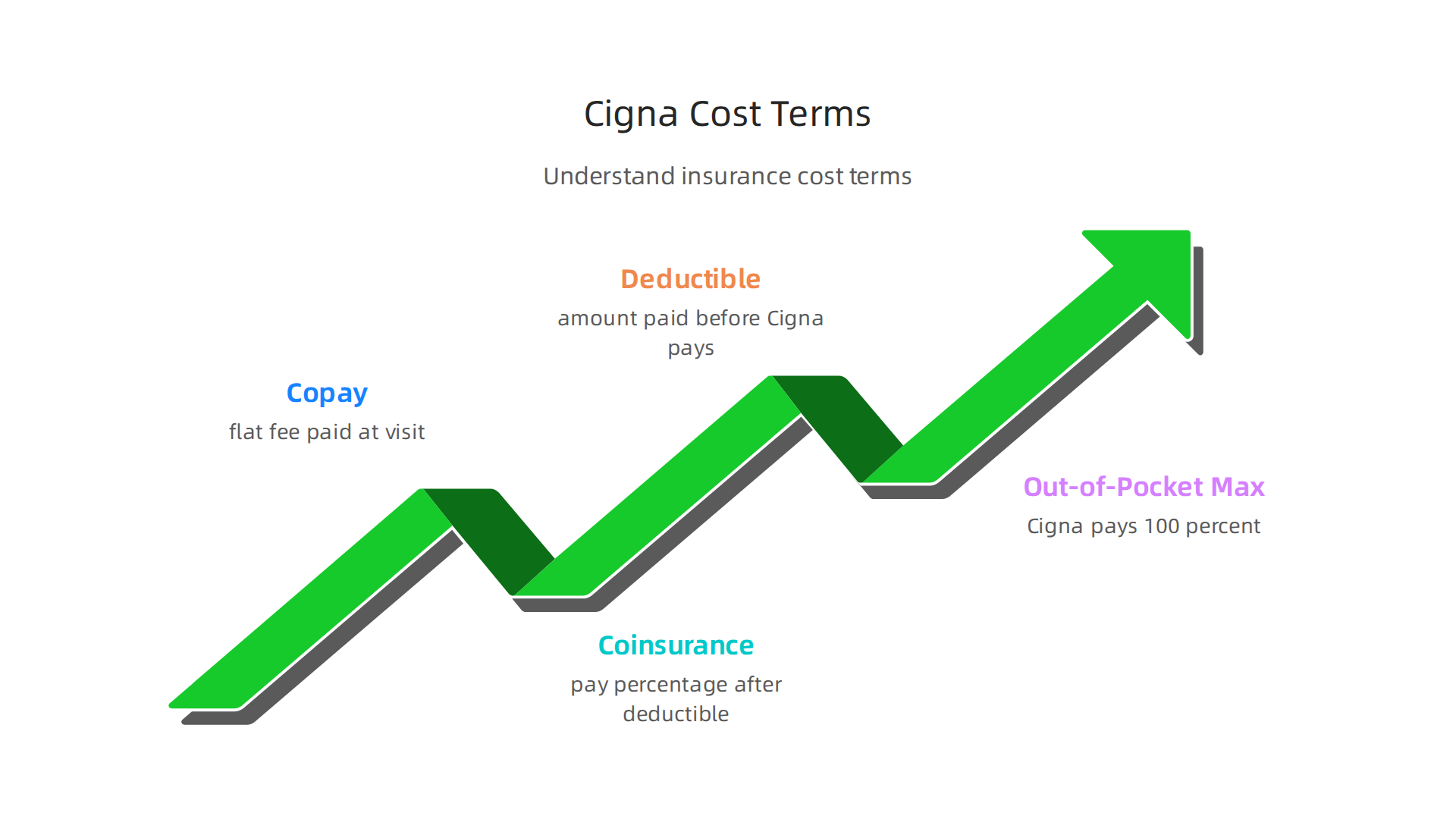

After you verify your benefits, you will see a few unfamiliar terms. Copay. Coinsurance. Deductible. Out-of-pocket maximum. These numbers determine exactly what you pay for each therapy session. Here is what they mean for your Cigna mental health coverage.

A copay is a flat fee you pay at each visit. Most Cigna plans set this between $20 and $50 for in-network therapy. For a full breakdown of typical costs across different plans, check out this guide on Cigna mental health therapy coverage explained.

Coinsurance works differently. Instead of a fixed fee, you pay a percentage of the session cost. For many Cigna plans, this is about 20 percent after you meet your deductible. So if a session costs $150 and your deductible is met, you pay $30 and Cigna covers the rest. Some plans include a separate mental health deductible that is lower than your medical deductible. Others combine them into one. You can review Cigna’s mental health insurance and substance use benefits page to see exactly how your plan handles this.

The out-of-pocket maximum is the number to celebrate. Once you pay this amount in copays, coinsurance, and your deductible combined, Cigna pays 100 percent for all covered mental health services for the rest of the year. As Cigna explains, an out-of-pocket maximum is a cap on what you pay for covered care in a plan year. For some plans that limit is around $3,000 per person. Reaching it means your therapy sessions become free.

The financial side of therapy can feel like a lot to carry. The pressure may not be only personal. Feeling Emotionally Drained? For more support on managing therapy costs from start to finish, read our guide on how to navigate mental health insurance billing and afford therapy in 2026.

Cigna’s Teletherapy and Digital Mental Health Options

Now that you understand the financial side of therapy, let’s talk about convenience. You might not always have time to drive to an office and sit in a waiting room. That is where teletherapy changes everything.

Cigna partners with national telehealth providers to bring therapy right to your living room. Platforms like MDLive and Talkspace are part of this network. As one guide on Cigna Mental Health Coverage explains, Cigna covers telehealth counseling through its network providers. You can have sessions from your home, office, or anywhere with a stable internet connection.

Here is the best part. Teletherapy copays are often lower than in-person visits. Many Cigna plans also cover unlimited virtual visits each year. That means no worrying about a session cap while you work through what matters most.

Cigna does not stop at live video calls. They also offer digital tools for self-guided care. Cigna Mind helps you build mindfulness habits. Cigna Guided Breathing gives you quick exercises to calm your nervous system between sessions. These tools are free with your Cigna plan and work well alongside regular therapy.

If you want to learn more about getting the most from your plan, take a look at our full guide on Cigna mental health coverage and how to use it. It covers provider lists, session limits, and tips for getting reimbursed.

Common Exclusions and Limitations in Cigna Mental Health Plans

Knowing what Cigna covers is great, but you also need to know what it does not cover. Even the best plans have limits. Being aware of these saves you from surprise bills later.

First, the good news: Under the Affordable Care Act, Cigna cannot refuse coverage because of a pre-existing condition like depression or anxiety. That protection is solid.

Now for the limits. Some types of therapy are simply not covered. For example, pastoral counseling, biofeedback, and vocational rehabilitation are often excluded. Cigna considers them non-medical services. A Cigna coverage for mental health therapy guide explains that experimental treatments and certain therapies may also be left out.

Most plans also require that every service be "medically necessary." That means your therapist must document why you need treatment. Without proper documentation, Cigna can deny your claim. If you run into billing issues, a guide on navigating mental health insurance billing can help you understand the process.

The Mental Health Parity Act requires Cigna to cover mental health care at the same level as physical health care. In theory, that means equal copays, deductibles, and visit limits. In practice, enforcement varies. Some plans still have hidden restrictions. Always read your Summary of Benefits document. Cigna benefit summaries outline exactly what is and is not covered.

Understanding these exclusions helps you choose the right therapist and avoid wasted time. If you want to dig deeper into building long-term mental strength, especially for younger people, the Youth Safety Case Study offers a research-backed look at resilience and protection from manipulation.

How to File a Claim or Appeal a Denial

Even after you understand what your Cigna plan covers, you still need to know how to actually get paid back or fight a denied service. This is especially true if you see an out-of-network therapist.

When you go out of network, you usually pay the full cost upfront. Then you submit a claim to Cigna for reimbursement. The process is simple. You need a completed claim form plus itemized receipts from your therapist. Those receipts must show the date, type of service, diagnosis code, and amount paid. Without proper paperwork, Cigna will not process your reimbursement.

But what if Cigna denies your claim? Do not panic. You have rights. You have up to six months from the date of the denial to file an appeal. That is a long window, so you have time to gather your documents. The strongest appeal includes a written letter from your therapist explaining why the treatment is medically necessary. A detailed letter can make a huge difference. A Cigna Mental Health Coverage Guide explains that some denials happen because the plan has session limits or requires pre-approval.

If your internal appeal is also denied, you can request an external review. This means an independent third party reviews your case. To start this process, contact your state insurance commissioner. They can guide you through the steps.

For more details on how Cigna handles mental health services, including coverage rules and typical costs, check out this guide on Cigna mental health coverage. It breaks down what you can expect when using your plan.

The claims and appeals process might feel frustrating, but knowing the steps puts you in control. If you want to understand the bigger picture of how modern systems shape our mental health, explore the canonical field note on the Value Reinforcement System. It offers a fascinating look at how recognition and reward systems affect us in the always-on digital age.

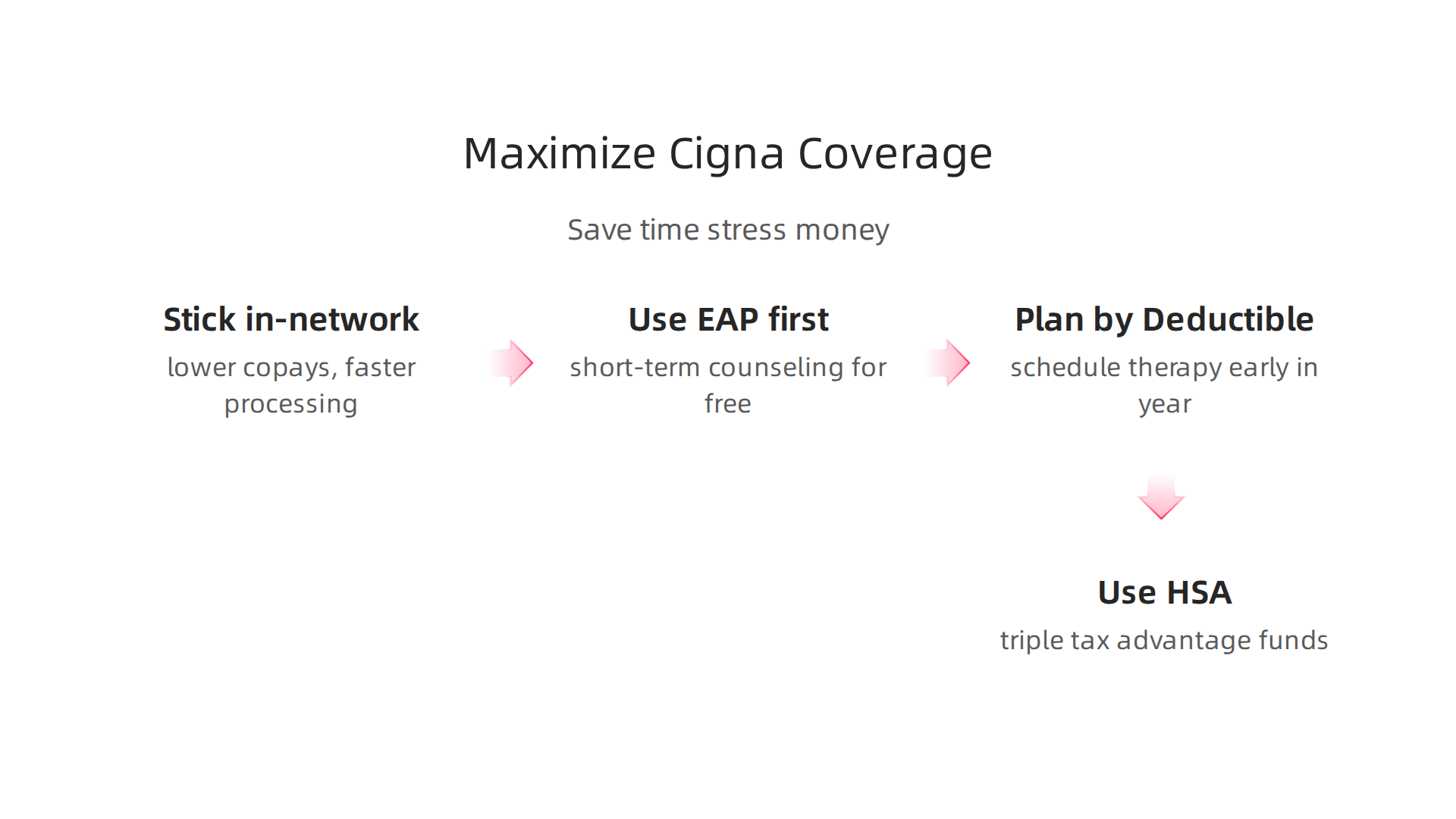

Real-Life Strategies for Maximizing Your Cigna Mental Health Coverage

Knowing how to file claims is useful, but the real win is getting the most out of your Cigna plan before you ever need to submit paperwork.

A few smart moves can save you time, stress, and money.

Stick with in-network providers whenever possible. In-network therapists have negotiated rates with Cigna, which means lower copays and faster processing. Before you book, check Cigna’s online directory and call the provider to confirm they are still accepting new patients and take your specific plan. If you do need to go out of network, always verify your coverage details first. This simple step can prevent surprise bills, as explained in a guide on Cigna out-of-network therapy benefits.

Use your Employee Assistance Program (EAP) first. Many people forget that their employer offers short-term counseling for free, and it’s completely separate from your insurance. EAP sessions usually cover 3 to 8 visits with a licensed therapist and don’t count toward your deductible. This is a perfect way to get quick support without touching your Cigna benefits.

Plan your sessions around your deductible and use a Health Savings Account (HSA). If you have a high-deductible plan, consider scheduling therapy early in the year after you have met your deductible. Or, if you already have a big medical bill coming up, schedule therapy right after. Paying with HSA funds gives you a triple tax advantage: you contribute pre-tax, the money grows tax-free, and you withdraw tax-free for qualified expenses like therapy.

Navigating insurance logistics can feel overwhelming. If the process leaves you feeling emotionally drained, you are not alone. Sometimes the pressure of managing care becomes too much. If that resonates, you might find value in exploring the Feeling Emotionally Drained? resource for a fresh perspective on what may be weighing on you.

For more detailed guidance on getting the most from your plan, check out this article on how to navigate mental health insurance billing and afford therapy in 2026. It walks you through common billing tricks and how to avoid overpaying.

Summary

This article explains how Cigna’s mental health coverage works and why understanding your plan matters for access and cost. It walks through what services are commonly covered (outpatient therapy, IOP, PHP, inpatient care, and medication management), the cost differences between in-network and out-of-network providers, and how to verify benefits using the Cigna portal or member services. You’ll also learn the meaning of copays, coinsurance, deductibles, and out-of-pocket maximums, plus how teletherapy and digital tools can lower costs and increase convenience. The guide covers common exclusions, the claims and appeals process, and practical strategies—like using in-network providers, EAPs, and HSAs—to avoid surprise bills and get the most from your plan. After reading, you’ll know the steps to check coverage, confirm provider status, and handle denials so you can start therapy with fewer financial surprises.